Actinium-Based Radiopharmaceuticals in 2025: Transforming Targeted Cancer Therapy and Unlocking Rapid Market Expansion. Explore the Innovations, Key Players, and Forecasts Shaping the Next Era of Precision Oncology.

- Executive Summary: 2025 Market Snapshot & Key Takeaways

- Technology Overview: Actinium-225 and Radiopharmaceutical Mechanisms

- Current Clinical Pipeline and Regulatory Milestones

- Key Players and Strategic Partnerships (e.g., actiniumpharma.com, bayer.com)

- Market Size, Segmentation, and 2025–2030 Growth Forecasts

- Manufacturing, Supply Chain, and Isotope Production Challenges

- Competitive Landscape and Emerging Entrants

- Applications in Oncology: Indications, Efficacy, and Patient Impact

- Investment Trends, M&A Activity, and Funding Outlook

- Future Outlook: Innovation Drivers, Unmet Needs, and Projected CAGR (2025–2030)

- Sources & References

Executive Summary: 2025 Market Snapshot & Key Takeaways

The global market for actinium-based radiopharmaceuticals is poised for significant growth in 2025, driven by advances in targeted alpha therapy (TAT), increasing clinical trial activity, and expanding production capabilities. Actinium-225, a potent alpha-emitting isotope, is at the forefront of this sector due to its high linear energy transfer and short path length, making it ideal for selectively destroying cancer cells while minimizing damage to healthy tissue.

In 2025, the demand for actinium-225 continues to outpace supply, with major pharmaceutical and radiopharmaceutical companies investing in new production technologies and partnerships. Curium, a global leader in nuclear medicine, has announced ongoing investments to scale up actinium-225 production, aiming to address the bottleneck in isotope availability. Similarly, IONETIX Corporation is expanding its cyclotron-based production infrastructure in the United States, targeting both clinical and commercial supply for investigational and approved therapies.

On the clinical front, several late-stage trials are underway for actinium-225-labeled therapeutics, particularly in prostate cancer and hematological malignancies. Actinium Pharmaceuticals remains a key player, advancing its Iomab-B program for conditioning in bone marrow transplant, with pivotal data expected in 2025. The company is also exploring additional indications and combination regimens, reflecting the broader trend of pipeline diversification in the sector.

Regulatory momentum is building, with agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) providing guidance on the development and approval of alpha-emitting radiopharmaceuticals. This regulatory clarity is expected to accelerate market entry for new therapies and foster greater investment in manufacturing infrastructure.

Key takeaways for 2025 include:

- Supply chain constraints for actinium-225 remain a challenge, but new production initiatives by companies like Curium and IONETIX Corporation are expected to improve availability in the near term.

- Clinical momentum is strong, with multiple phase II/III trials ongoing and potential first approvals for actinium-225-based therapies anticipated within the next few years.

- Strategic collaborations between isotope producers, pharmaceutical developers, and healthcare providers are intensifying, aiming to streamline the path from isotope production to patient treatment.

- Market outlook for 2025 and beyond is robust, with actinium-based radiopharmaceuticals positioned as a transformative modality in precision oncology and rare disease treatment.

Overall, 2025 marks a pivotal year for actinium-based radiopharmaceuticals, with the sector transitioning from early-stage innovation to broader clinical adoption and commercial scale-up.

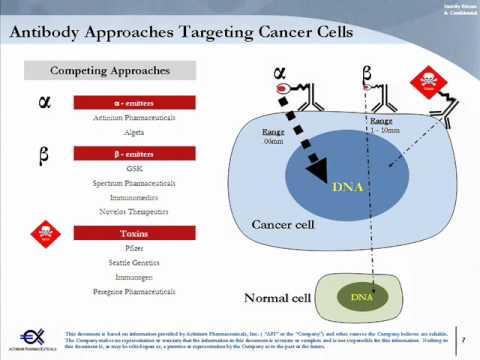

Technology Overview: Actinium-225 and Radiopharmaceutical Mechanisms

Actinium-based radiopharmaceuticals, particularly those utilizing the isotope Actinium-225 (Ac-225), are at the forefront of next-generation targeted alpha therapy (TAT) for cancer treatment. Ac-225 is a potent alpha emitter with a half-life of approximately 10 days, making it highly suitable for delivering cytotoxic radiation directly to malignant cells while minimizing damage to surrounding healthy tissue. The mechanism involves conjugating Ac-225 to tumor-targeting molecules, such as monoclonal antibodies or peptides, which selectively bind to cancer cell markers. Upon internalization, the decay of Ac-225 releases high-energy alpha particles, inducing irreparable double-strand DNA breaks and leading to cell death.

The current landscape in 2025 is marked by significant advancements in both the production and clinical application of Ac-225 radiopharmaceuticals. Historically, limited global supply of Ac-225 has constrained clinical development. However, several organizations have made notable progress in scaling up production. Orano Med, a subsidiary of Orano Group, is a leading player with dedicated facilities in France and the United States, focusing on the industrial-scale production of Ac-225 and the development of proprietary TAT candidates. Similarly, IONETIX Corporation has established cyclotron-based production capabilities in the U.S., aiming to address supply bottlenecks and support clinical trials.

On the pharmaceutical front, multiple companies are advancing Ac-225-labeled therapeutics through clinical pipelines. Actinium Pharmaceuticals is a pioneer in this space, with its lead candidate Iomab-B (I-131, but with ongoing research into Ac-225 conjugates) and a robust pipeline of Ac-225-based agents targeting hematologic malignancies and solid tumors. Bayer AG is also investing in alpha therapy platforms, leveraging its experience with radiopharmaceuticals such as Xofigo (Ra-223) and expanding into Ac-225-based assets through collaborations and acquisitions.

The outlook for 2025 and the coming years is optimistic, with expectations of increased clinical trial activity and potential regulatory submissions for Ac-225-based therapies. The U.S. Department of Energy’s Isotope Program is ramping up efforts to ensure a reliable domestic supply of Ac-225, which is anticipated to further accelerate research and commercialization. Additionally, advances in chelation chemistry and targeting vectors are enhancing the stability and specificity of Ac-225 radiopharmaceuticals, broadening their therapeutic window and potential indications.

In summary, the convergence of improved isotope availability, innovative targeting strategies, and growing clinical evidence positions actinium-based radiopharmaceuticals as a transformative modality in oncology, with several key players and infrastructure investments shaping the field’s trajectory through 2025 and beyond.

Current Clinical Pipeline and Regulatory Milestones

The clinical pipeline for actinium-based radiopharmaceuticals has expanded rapidly as of 2025, driven by the unique therapeutic potential of actinium-225 (Ac-225) in targeted alpha therapy (TAT). Actinium-225’s high linear energy transfer and short path length make it particularly effective for selectively destroying cancer cells while minimizing damage to surrounding healthy tissue. This has spurred a wave of clinical development, with several candidates advancing through early- and mid-stage trials.

Among the most prominent players, Actinium Pharmaceuticals, Inc. continues to lead with its flagship candidate Iomab-B, an Ac-225-labeled anti-CD45 antibody for conditioning in bone marrow transplant. Iomab-B completed a pivotal Phase 3 trial in 2023, and the company submitted a Biologics License Application (BLA) to the U.S. Food and Drug Administration (FDA) in late 2024. A regulatory decision is anticipated in 2025, which could mark the first approval of an actinium-based radiopharmaceutical for hematologic malignancies in the U.S.

Another key developer, Bayer AG, is advancing Ac-225-labeled PSMA-targeted agents for metastatic castration-resistant prostate cancer (mCRPC). Bayer’s radiopharmaceutical division, building on its experience with Xofigo (radium-223), has initiated Phase 1/2 trials for its Ac-225-PSMA compound, with initial safety and efficacy data expected in 2025. The company is also investing in production scale-up to address anticipated supply constraints for Ac-225.

Meanwhile, Orano Med is progressing with its lead candidate, Ac-225-labeled DOTATOC, targeting neuroendocrine tumors. Orano Med has established a vertically integrated supply chain for Ac-225, and its clinical program includes multiple Phase 1/2 studies in Europe and North America. The company is also collaborating with academic centers to expand indications and optimize dosing regimens.

On the regulatory front, both the U.S. FDA and the European Medicines Agency (EMA) have signaled increased support for radiopharmaceutical innovation, including expedited pathways for therapies addressing high unmet needs. In 2024, the FDA granted Fast Track designation to several actinium-based candidates, reflecting the agency’s recognition of their potential. The EMA has similarly provided Priority Medicines (PRIME) status to select programs, facilitating earlier engagement and guidance.

Looking ahead, the next few years are expected to see pivotal trial readouts, potential first approvals, and further expansion of the clinical pipeline. The sector’s outlook is buoyed by growing investment in Ac-225 production capacity, with companies such as Nordion and Curium scaling up isotope supply to meet anticipated clinical and commercial demand. As regulatory milestones are achieved, actinium-based radiopharmaceuticals are poised to become a cornerstone of targeted cancer therapy.

Key Players and Strategic Partnerships (e.g., actiniumpharma.com, bayer.com)

The landscape of actinium-based radiopharmaceuticals is rapidly evolving, with several key players and strategic partnerships shaping the sector as of 2025 and looking ahead. Actinium-225, a potent alpha-emitting isotope, is at the center of these developments due to its promising therapeutic potential in targeted alpha therapy (TAT) for various cancers.

One of the most prominent companies in this field is Actinium Pharmaceuticals, Inc., which has established itself as a leader in the development of actinium-225-based therapies. Their flagship program, Iomab-B, is in advanced clinical stages for conditioning in bone marrow transplant, and the company is actively expanding its pipeline to include other actinium-labeled candidates for hematologic and solid tumors. Actinium Pharmaceuticals has also entered into collaborations with major academic centers and pharmaceutical companies to accelerate clinical development and broaden the application of actinium-225.

Another significant player is Bayer AG, which has a strong presence in radiopharmaceuticals through its established radiotherapeutic, Xofigo (radium-223). Bayer is investing in next-generation alpha therapies, including actinium-225, and has announced partnerships with biotech firms and isotope suppliers to secure reliable actinium-225 supply and develop new targeted radiotherapeutics. Bayer’s strategic moves are expected to drive further innovation and commercialization in the actinium-based space over the next few years.

The reliable supply of actinium-225 remains a critical bottleneck for the industry. Curium, a global leader in nuclear medicine, is actively investing in the production and distribution of actinium-225, leveraging its expertise in isotope manufacturing and logistics. Curium’s efforts are complemented by partnerships with both pharmaceutical developers and government agencies to scale up production capacity and ensure a stable supply chain for clinical and commercial needs.

Other notable companies include Orano, which is expanding its radiopharmaceutical portfolio to include actinium-225, and NorthStar Medical Radioisotopes, which is developing proprietary production technologies to meet the growing demand for high-purity actinium-225. These companies are forming strategic alliances with research institutions and pharmaceutical firms to accelerate the translation of actinium-based therapies from bench to bedside.

Looking forward, the next few years are expected to see intensified collaboration between isotope producers, pharmaceutical developers, and healthcare providers. These partnerships are crucial for overcoming supply challenges, advancing clinical trials, and ultimately bringing novel actinium-225 radiopharmaceuticals to market, with the potential to transform cancer therapy paradigms.

Market Size, Segmentation, and 2025–2030 Growth Forecasts

The global market for actinium-based radiopharmaceuticals is poised for significant expansion between 2025 and 2030, driven by advances in targeted alpha therapy (TAT), increasing clinical trial activity, and growing investment in radiotherapeutics manufacturing infrastructure. Actinium-225, in particular, is gaining prominence as a potent alpha-emitting isotope for cancer therapy, with a focus on hematologic malignancies and solid tumors.

As of 2025, the actinium-based radiopharmaceuticals market remains in an early but rapidly evolving stage. The number of clinical trials involving actinium-225-labeled agents has increased, with several candidates advancing into late-stage development. Notably, Actinium Pharmaceuticals, Inc. is a leading developer, with its Iomab-B (I-131 apamistamab) and Actimab-A (actinium-225 lintuzumab) programs targeting hematologic cancers. The company is also expanding its pipeline to include solid tumor indications. Another key player, Curium, is investing in the production and supply of actinium-225, aiming to support both clinical and commercial demand.

The market is segmented by isotope (primarily actinium-225), application (hematologic malignancies, solid tumors, and others), and end user (hospitals, specialty clinics, and research institutions). The hematologic malignancies segment currently dominates, but the solid tumor segment is expected to grow rapidly as more actinium-225-based agents enter clinical trials for prostate, neuroendocrine, and other cancers.

Production capacity remains a critical bottleneck. Historically, actinium-225 supply has been limited, but recent investments are addressing this challenge. NorthStar Medical Radioisotopes and IONETIX Corporation are scaling up cyclotron and generator-based production methods, with the goal of supporting commercial-scale radiopharmaceutical manufacturing by the late 2020s. TerraPower is also collaborating with government and industry partners to expand isotope availability.

Looking ahead, the actinium-based radiopharmaceuticals market is forecast to achieve double-digit compound annual growth rates (CAGR) through 2030, with estimates ranging from $500 million to over $1 billion in annual revenues by the end of the decade, depending on regulatory approvals and production scalability. The entry of new suppliers and the expansion of clinical indications are expected to further accelerate market growth. Strategic partnerships between pharmaceutical companies, isotope producers, and healthcare providers will be crucial in overcoming supply chain and regulatory hurdles, ensuring that actinium-based therapies reach broader patient populations in the coming years.

Manufacturing, Supply Chain, and Isotope Production Challenges

The manufacturing and supply chain landscape for actinium-based radiopharmaceuticals is undergoing rapid transformation as the sector prepares for anticipated clinical and commercial demand in 2025 and beyond. Actinium-225 (Ac-225), the key isotope for targeted alpha therapy (TAT), remains in critically short supply, with global annual production estimated at only a few curies—far below projected needs for late-stage clinical trials and potential market launches.

Historically, Ac-225 has been sourced primarily from the decay of thorium-229 stocks, a legacy of past nuclear programs. This method, however, is limited by the finite availability of thorium-229, constraining the scalability of Ac-225 production. In response, several organizations are investing in alternative production routes, including proton irradiation of radium-226 targets and high-energy accelerator-based methods. For example, Orano and Curium—both major nuclear medicine suppliers—have announced initiatives to expand Ac-225 production capacity using cyclotron and linear accelerator technologies. These efforts are expected to yield multi-curie annual outputs within the next few years, though technical and regulatory hurdles remain.

In North America, Nordion and BWX Technologies are advancing proprietary processes for Ac-225 generation, leveraging their expertise in isotope production and radiopharmaceutical supply chains. BWX Technologies in particular has reported progress on scaling up Ac-225 output at its facilities, with the goal of supporting both clinical research and commercial supply by 2025. Meanwhile, Nordion is collaborating with government and academic partners to optimize target materials and purification protocols, aiming to ensure reliable, high-purity isotope delivery.

The supply chain for actinium-based radiopharmaceuticals is further complicated by the isotope’s short half-life (10 days), necessitating just-in-time logistics and robust coordination between producers, radiopharmacies, and clinical sites. Companies such as Curium and Orano are investing in specialized packaging, rapid transport solutions, and digital tracking systems to minimize decay losses and ensure product integrity.

Looking ahead, the sector anticipates a gradual easing of supply constraints as new production facilities come online and regulatory frameworks adapt to the unique challenges of alpha-emitting isotopes. However, the pace of clinical development and potential regulatory approvals for actinium-based therapies will continue to exert pressure on the supply chain. Strategic partnerships, public-private collaborations, and continued investment in isotope production infrastructure will be critical to meeting the needs of patients and advancing the field of targeted alpha therapy in the coming years.

Competitive Landscape and Emerging Entrants

The competitive landscape for actinium-based radiopharmaceuticals is rapidly evolving as the global demand for targeted alpha therapies (TATs) intensifies. Actinium-225, prized for its potent alpha-emitting properties and short path length, is at the center of this innovation wave, particularly for oncology indications such as prostate, neuroendocrine, and hematologic cancers. As of 2025, the sector is characterized by a mix of established radiopharmaceutical companies, emerging biotech entrants, and strategic collaborations aimed at overcoming production bottlenecks and accelerating clinical development.

Among the established players, Bayer AG continues to leverage its radiopharmaceutical expertise, building on the commercial success of Xofigo (radium-223) and investing in next-generation actinium-based assets. Novartis AG, following its acquisitions of Advanced Accelerator Applications and Endocyte, is actively expanding its radioligand therapy pipeline, with several actinium-225 programs in preclinical and early clinical stages. Curium Pharma, a global leader in nuclear medicine, is also investing in actinium-225 supply and radiopharmaceutical development, aiming to secure a foothold in the TAT market.

Emerging entrants are playing a pivotal role in shaping the competitive dynamics. Actinium Pharmaceuticals, Inc. is advancing Iomab-B (I-131) and Actimab-A (actinium-225-lintuzumab) for hematologic malignancies, with Actimab-A in multiple clinical trials. POINT Biopharma Global Inc. is developing a pipeline of actinium-225 and lutetium-177 radioligand therapies, with a focus on scalable manufacturing and rapid clinical translation. Telix Pharmaceuticals Limited is also entering the actinium space, leveraging its global radiopharmaceutical distribution network.

A critical competitive factor is the reliable supply of actinium-225, which remains a bottleneck due to limited global production capacity. Nordion (Canada) Inc. and IONETIX Corporation are among the few commercial suppliers scaling up production, while government-backed initiatives in North America and Europe are supporting new production routes to meet anticipated demand.

Looking ahead to the next few years, the sector is expected to see increased M&A activity, strategic partnerships, and vertical integration as companies seek to secure isotope supply chains and accelerate clinical development. The entry of large pharmaceutical companies and the maturation of emerging biotech players are likely to intensify competition, drive innovation, and expand patient access to actinium-based radiopharmaceuticals globally.

Applications in Oncology: Indications, Efficacy, and Patient Impact

Actinium-based radiopharmaceuticals, particularly those utilizing the alpha-emitting isotope actinium-225 (Ac-225), are at the forefront of innovation in targeted cancer therapy as of 2025. These agents deliver potent cytotoxic radiation directly to tumor cells, minimizing damage to surrounding healthy tissue. The most prominent application is in the treatment of advanced prostate cancer, specifically metastatic castration-resistant prostate cancer (mCRPC), where actinium-225-labeled prostate-specific membrane antigen (PSMA) ligands have shown remarkable efficacy in early clinical studies. Patients with mCRPC who have exhausted conventional therapies have demonstrated significant reductions in prostate-specific antigen (PSA) levels and radiographic tumor burden following treatment with Ac-225-PSMA compounds.

Several companies are leading the development and clinical translation of actinium-based radiopharmaceuticals. Bayer AG is advancing its pipeline with investigational Ac-225 radioligands, building on its established expertise in radiopharmaceuticals. Novartis AG, following its acquisition of Advanced Accelerator Applications and Endocyte, is conducting pivotal trials of Ac-225-PSMA-617, aiming to expand indications beyond prostate cancer. POINT Biopharma Global Inc. is also actively developing actinium-based agents for a range of solid tumors, including neuroendocrine tumors and small cell lung cancer, with several candidates in early-phase clinical trials.

The efficacy of actinium-based therapies is underpinned by the high linear energy transfer (LET) of alpha particles, which induces irreparable double-strand DNA breaks in cancer cells. Early-phase clinical data suggest that Ac-225 radiopharmaceuticals can achieve objective response rates exceeding 50% in heavily pretreated mCRPC patients, with some experiencing durable remissions. However, challenges such as xerostomia (dry mouth) due to salivary gland uptake and hematologic toxicity remain areas of active investigation, with ongoing efforts to optimize dosing and delivery.

Looking ahead, the next few years are expected to see the expansion of actinium-based radiopharmaceuticals into additional oncologic indications, including hematologic malignancies and other solid tumors expressing suitable molecular targets. The anticipated increase in global Ac-225 supply, driven by investments from companies such as Nordion and Curium, is poised to accelerate clinical research and broaden patient access. As regulatory approvals are pursued, actinium-based radiopharmaceuticals are positioned to become a transformative modality in precision oncology, offering new hope for patients with otherwise limited treatment options.

Investment Trends, M&A Activity, and Funding Outlook

The actinium-based radiopharmaceuticals sector is experiencing a surge in investment and strategic activity as the global demand for targeted alpha therapies intensifies. In 2025, the market is characterized by robust funding rounds, increased mergers and acquisitions (M&A), and a growing number of partnerships aimed at securing supply chains and accelerating clinical development. This momentum is driven by the unique therapeutic potential of actinium-225, which offers highly potent, targeted cancer cell destruction with minimal damage to surrounding healthy tissue.

Key players such as Curium, Orano Med, and POINT Biopharma are at the forefront of these developments. Curium has made significant investments in expanding its actinium-225 production capabilities, aiming to address the global shortage of this critical isotope. In parallel, Orano Med continues to advance its proprietary Targeted Alpha Therapy (TAT) platform, supported by strategic funding and collaborations with academic and clinical partners. POINT Biopharma has also attracted substantial capital to accelerate its actinium-based clinical pipeline, reflecting investor confidence in the sector’s growth prospects.

M&A activity is intensifying as established pharmaceutical companies seek to enter or expand their presence in the radiopharmaceuticals market. Recent years have seen a wave of acquisitions and joint ventures, with large players targeting innovative startups and technology holders. This trend is expected to continue through 2025 and beyond, as companies aim to secure access to actinium-225 supply and proprietary delivery technologies. For example, Curium and Orano Med have both engaged in strategic partnerships to strengthen their clinical and manufacturing capabilities.

On the funding front, venture capital and institutional investors are increasingly active, drawn by the sector’s high growth potential and the expanding pipeline of actinium-based therapies. Several companies have announced multi-million dollar funding rounds in 2024 and early 2025, earmarked for scaling up isotope production, advancing clinical trials, and building out commercial infrastructure. Governmental and public-private initiatives are also playing a role, with agencies in North America and Europe supporting domestic actinium-225 production to reduce reliance on limited global sources.

Looking ahead, the outlook for investment and M&A in actinium-based radiopharmaceuticals remains highly positive. As clinical data matures and regulatory pathways become clearer, the sector is poised for further consolidation and capital inflows. The next few years are likely to see continued strategic activity, with a focus on securing supply chains, expanding therapeutic indications, and accelerating commercialization of actinium-based therapies.

Future Outlook: Innovation Drivers, Unmet Needs, and Projected CAGR (2025–2030)

The future outlook for actinium-based radiopharmaceuticals is shaped by a convergence of innovation drivers, persistent unmet clinical needs, and robust market growth projections for the period 2025–2030. Actinium-225, a potent alpha-emitting isotope, is at the forefront of targeted alpha therapy (TAT), offering the potential for highly selective cancer cell destruction with minimal damage to surrounding healthy tissue. This unique therapeutic profile is fueling significant R&D investment and strategic collaborations among leading radiopharmaceutical companies and nuclear technology suppliers.

A primary innovation driver is the increasing clinical validation of actinium-225–labeled agents in late-stage oncology trials, particularly for hematologic malignancies and metastatic solid tumors. Companies such as Bayer AG and Novartis AG are advancing actinium-based candidates through their pipelines, building on the commercial and clinical momentum established by earlier radioligand therapies. Orano Med, a subsidiary of Orano Group, is also a key player, focusing on the development and production of lead-212 and actinium-225 radiopharmaceuticals, with several clinical programs underway.

A critical bottleneck remains the limited global supply of actinium-225, which is currently produced in small quantities via legacy thorium generators or cyclotron-based methods. To address this, organizations such as Nordion and Curium are investing in new production technologies and infrastructure, aiming to scale up isotope availability to meet anticipated clinical and commercial demand. The U.S. Department of Energy’s Isotope Program is also expanding domestic production capacity, which is expected to alleviate supply constraints and accelerate clinical development timelines.

Unmet needs in the oncology landscape—particularly for patients with relapsed or refractory cancers—are driving demand for novel therapies with improved efficacy and safety profiles. Actinium-based radiopharmaceuticals are uniquely positioned to address these gaps, especially in indications where conventional therapies have limited impact. The next few years are expected to see a wave of pivotal trial readouts, regulatory submissions, and potential product launches, further validating the clinical and commercial potential of this modality.

Market analysts and industry stakeholders project a strong compound annual growth rate (CAGR) for the actinium-based radiopharmaceutical sector, with estimates commonly ranging from 25% to 35% for 2025–2030, driven by expanding clinical indications, increased isotope supply, and growing adoption in major healthcare markets. As innovation accelerates and supply chain challenges are addressed, actinium-based radiopharmaceuticals are poised to become a cornerstone of precision oncology in the coming decade.

Sources & References

- Curium

- IONETIX Corporation

- Actinium Pharmaceuticals

- Orano Med

- IONETIX Corporation

- Actinium Pharmaceuticals

- Curium

- Orano

- NorthStar Medical Radioisotopes

- Orano

- Novartis AG